Digital Banking Competition in Southeast Asia Should Intensify as there’s been a Boom in Fintech Investments

Updated On : December 2020

As per the Fitch Ratings report, in Southeast Asia, the unbanked population is around 290 million. The report says that only 18 percentage of the population in SE Asia has access to credit which is lower than the proportion of the digital-ready population, 37 percentage based on World Bank Global Findex data.

The Association of Southeast Asian Nations (ASEAN) is a group consisting of Cambodia, Brunei, Indonesia, Laos, Malaysia, Singapore, Myanmar, the Philippines, Thailand, and Vietnam. According to Fitch ratings, the Philippines and Indonesia have a large market potential amongst the six major ASEAN markets, because of their large unbanked segment.

Major Investments in Southeast Asia

- According to the Q2 APAC funding report by S&P Global Market Intelligence, the Investments in Asia-Pacific has grown to 9.1% i.e. US $ 1.4 billion in 2020 as compared to the first quarter

- The fintech funding in Asia was led by South East Asia and Australia, both regions drew the US $ 455 million and the US $ 369 million which is around three times and two times the amount raised in the previous quarter respectively

- As per the Future Fintech Southeast Asia report conducted by Dealroom, Finch Capital, and MDI Ventures, the foreign investment into fintech companies in SE Asia has grown seven times. Some of the active investors are Tencent, Ant Financial, Sequoia, Accel, SoftBank, and Warburg Pincus

Opportunities in Southeast Asia

- Southeast Asia has a population of 570 million and a GDP is expected to reach $4.7 trillion by 2025. The financial sector holds tremendous potential if the large unbanked population is served and millions of SMEs funding gaps are filled

- Southeast Asia countries represent one of the world’s largest and fastest-growing regions

- Southeast Asia’s fintech startups are worth a combined US$10 billion, that includes Vietnam’s MoMo and VNPay, Indonesia’s, Akulaku, Ovo and PayFazz, and Singapore’s FinAccel, as per the report which is the most valued fintech start-ups at a valuation of above $ 250 million each

- The report says, with a booming internet economy, a large population of unbanked population, and around 22 million people joining the mobile age every year. Southeast Asia has a massive opportunity for both local and foreign fintech to grow.

Southeast Asia’s overall tech ecosystem estimated is currently worth the US $ 108 billion. Singapore, Indonesia, the Philippines, Vietnam, and Malaysia are some of the valuable tech ecosystems.

According to analysis, the fintech solutions will help to boost the financial inclusions and also help in increasing the GDP of emerging markets by $ 3.7 trillion. SE Asia has seen a boom in Fintech investments in recent years. The banking competition will increase as virtual banks will enter the market.

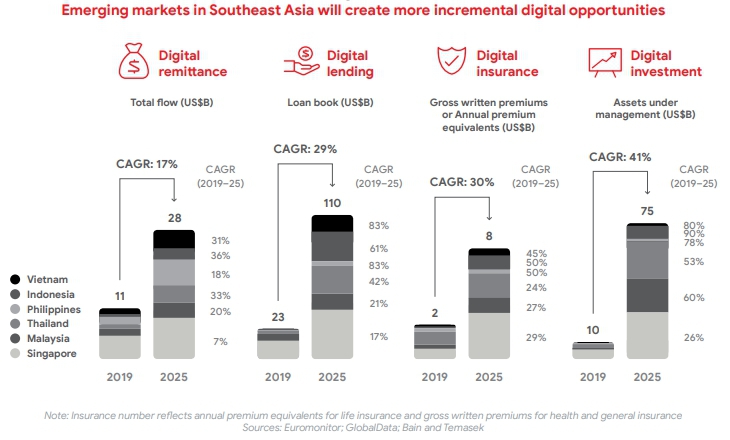

Southeast Asia’s developing markets are likely to show a growth in digital financial services. As per the report Vietnam, Indonesia and Philippines digital payments gross transaction value will grow by 10–13 percentage CAGR until 2025 v/s 3 percentage in Singapore. These three countries’ total amount of digital loans is expected to grow by more than 50% CAGR to 2025.

The COVID-19 pandemic may have affected the region’s economy, appropriate measures need to be taken by the government to address the challenges i.e. lack of access to digital financial services to local consumers and businesses.

By adopting Digital Banking services, banks and financial institutions can make banking simple, convenient, and available to the large unbanked population in Southeast Asia. Nelito’s FinCraftTM Digital Banking Suite helps financial institutions provide compelling digital banking experiences, and is designed to Attract, Engage, and Extend Customer Relationships. FincraftTM provides an Omni-Channel digital banking suite that consists of core banking, mobile banking, internet banking, and doorstep banking solutions. This enables the institutions to drive innovation and growth, provide seamless customer experience, achieve operational excellence, and gain a competitive advantage.

Leave Comments :

© Nelito Systems Pvt. Ltd. Terms & Privacy

Comments :